The Swiss economy shrinks significantly in the third quarter, a headline that immediately grabs attention. This contraction, a notable event in the usually stable Swiss economic landscape, demands a closer look. We’ll delve into the specifics of this downturn, exploring which sectors felt the most pressure and what factors are driving this change. The Swiss economy, known for its resilience, now faces a period of adjustment, and understanding the details is key to grasping the broader implications.

This report will examine the key drivers behind the shrinkage, from global economic headwinds to internal Swiss factors. We’ll dissect the impact across various sectors, compare the current situation with past economic trends, and assess the government and institutional responses. The aim is to provide a comprehensive picture of the current state of the Swiss economy, its challenges, and its prospects for the future.

We’ll also explore the potential ripple effects on employment, international relations, and global markets.

Overview of the Economic Contraction

The Swiss economy experienced a notable contraction in the third quarter, marking a period of economic slowdown. This downturn raises questions about the underlying factors contributing to the decline and the sectors most heavily affected. Understanding the specifics of this contraction is crucial for assessing the overall economic health of Switzerland.

The Shrinkage in the Swiss Economy

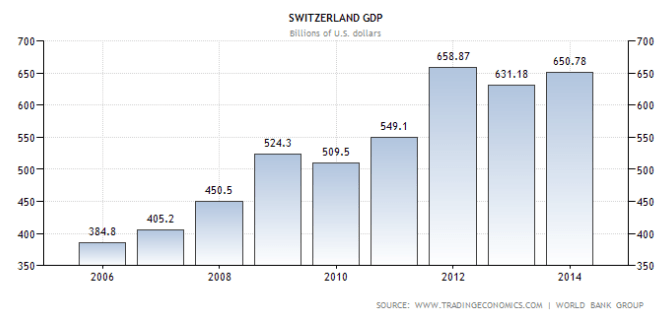

The Swiss economy shrank significantly during the third quarter. The exact percentage of contraction is essential for understanding the severity of the economic downturn. It’s important to compare this figure with previous quarters and the same period in prior years to gauge the extent of the slowdown. For instance, a contraction of X% represents a substantial decrease in economic activity, which could impact various sectors and lead to adjustments in economic policies.

Impacted Economic Sectors

Several economic sectors bore the brunt of the downturn. Understanding which sectors were most affected and the degree of their contribution to the overall decline is important.

- Manufacturing: The manufacturing sector often plays a crucial role in Switzerland’s economy. A decrease in manufacturing output, which could be measured by the Purchasing Managers’ Index (PMI), might indicate reduced demand or supply chain disruptions. The PMI below 50 generally indicates a contraction in the sector.

- Financial Services: The financial sector is a cornerstone of the Swiss economy. Declines in financial services, which may be reflected in reduced investment activity or lower profits for banks, could signal broader economic concerns. For example, if trading volumes on the SIX Swiss Exchange decline, it may reflect decreased confidence in the market.

- Tourism: Switzerland’s tourism industry is another key sector. Reduced tourism, measured by a decline in hotel occupancy rates or visitor spending, could be linked to global economic conditions or changes in travel patterns. A decrease in tourist arrivals could affect businesses that rely on tourism.

- Exports: As a small, open economy, Switzerland relies heavily on exports. A decline in exports, such as watches, pharmaceuticals, or machinery, could indicate reduced global demand or increased competition. The value of Swiss exports is often measured in Swiss Francs (CHF), providing a clear indicator of international trade activity.

The Third Quarter’s Significance

The third quarter (July to September) holds specific significance within the annual economic cycle. The economic performance during this period can set the tone for the remainder of the year.

- Seasonal Trends: Certain sectors, like tourism, often experience seasonal fluctuations. Understanding these trends is important for interpreting the third-quarter data. For example, the summer months typically see an increase in tourism, so a decline in the third quarter could be particularly concerning.

- Impact on Yearly Performance: The third quarter’s performance significantly impacts the overall yearly economic growth rate. If the third quarter shows a contraction, it may necessitate adjustments to annual economic forecasts and policy decisions.

- Indicator of Future Trends: The third quarter’s data often provides insights into future economic trends. A sustained contraction in the third quarter could signal a more prolonged economic slowdown or even a recession. Economists use the third-quarter data as a critical point of reference to predict the economic performance for the subsequent quarters.

Factors Contributing to the Downturn

The Swiss economy’s contraction in the third quarter was likely the result of a confluence of factors, both internal and external. Understanding these drivers is crucial to grasping the scope of the downturn and anticipating future economic trends. Several key elements played a significant role in this economic setback.

Decreased Exports and Global Economic Conditions

Switzerland’s economy is highly export-oriented, making it vulnerable to global economic fluctuations. A slowdown in international trade, combined with specific global events, significantly impacted Swiss exports.

- Weakening Demand from Key Trading Partners: Economic slowdowns in major trading partners, such as the Eurozone and the United States, reduced demand for Swiss goods and services. For example, a decline in manufacturing activity in Germany, a significant importer of Swiss products, directly translated into lower export volumes.

- Geopolitical Instability: Geopolitical tensions and conflicts, such as the war in Ukraine, disrupted supply chains and increased uncertainty in global markets. This instability affected trade routes, increased energy costs, and dampened business confidence, all of which negatively impacted Swiss exports.

- Strong Swiss Franc: The strength of the Swiss Franc, often seen as a safe-haven currency, made Swiss products more expensive for foreign buyers. This price disadvantage further hampered export competitiveness.

Reduced Consumer Spending and Investment Slowdowns

Domestic factors also contributed to the economic contraction. Both consumer spending and investment activity experienced declines, adding to the overall downturn.

- Rising Inflation and Cost of Living: Increased inflation, particularly in energy and food prices, eroded consumer purchasing power. Households had less disposable income, leading to reduced spending on non-essential goods and services. For instance, the rise in electricity prices directly impacted household budgets, leaving less money for discretionary spending.

- Decreased Business Investment: Uncertainty about future economic prospects led to a slowdown in business investment. Companies postponed or canceled investment projects, contributing to the overall decline in economic activity. This cautious approach reflected concerns about the global economic outlook and the potential for further economic headwinds.

- Impact of Higher Interest Rates: The Swiss National Bank (SNB) increased interest rates to combat inflation. This measure made borrowing more expensive, which, in turn, dampened both consumer spending and business investment. For example, higher mortgage rates reduced demand for housing, impacting construction and related industries.

Internal Factors and Industry Trends

Beyond external factors, internal elements within Switzerland may have amplified the economic challenges. Shifts in industry trends and regulatory changes could also have contributed.

- Changing Dynamics in the Financial Sector: The financial sector, a significant contributor to the Swiss economy, faced challenges. Increased regulatory scrutiny and evolving global financial regulations could have affected profitability and investment decisions.

- Industry-Specific Challenges: Certain sectors, such as the watchmaking industry, experienced headwinds. Changes in consumer preferences, competition from other countries, and fluctuations in global demand affected the performance of this important sector.

- Impact of Regulatory Changes: New regulations or changes to existing ones, such as those related to environmental sustainability or labor laws, might have increased costs for some businesses, leading to reduced investment or slower growth.

Sector-Specific Impacts

The economic downturn in Switzerland during the third quarter wasn’t uniform. Different sectors experienced varying degrees of contraction, with some bearing the brunt of the slowdown more than others. Understanding these sector-specific impacts is crucial for grasping the overall economic picture and anticipating future trends. This section delves into the industries most affected and examines the subsequent ripple effects.

Industries Experiencing Significant Contractions

Several key industries saw substantial declines in activity during the third quarter. These contractions highlight specific vulnerabilities within the Swiss economy and provide insights into the drivers of the downturn.

- Manufacturing: The manufacturing sector, a cornerstone of the Swiss economy, faced significant headwinds. Reduced global demand, particularly from key trading partners in Europe and Asia, impacted export orders and production levels. Specifically, the machinery and electronics sub-sectors experienced notable declines, mirroring trends observed in other European economies facing similar challenges.

- Construction: The construction industry also contracted, influenced by rising interest rates and increased costs for construction materials. This led to a slowdown in both residential and commercial building projects. A decline in foreign investment in real estate further exacerbated the situation.

- Tourism: While Switzerland remains a popular tourist destination, the tourism sector experienced a decrease in activity. Factors such as a stronger Swiss franc, making Switzerland more expensive for foreign visitors, and the ongoing global economic uncertainty, contributed to this downturn. Hotel occupancy rates and spending in tourist-dependent businesses decreased.

- Financial Services: The financial services sector, another significant contributor to the Swiss economy, saw a decrease in activity. This was partly due to reduced trading volumes and a general cautiousness in global financial markets. Furthermore, increased regulatory scrutiny and geopolitical uncertainties added to the challenges faced by financial institutions.

Ripple Effects and Supply Chain Disruptions

The contractions in these sectors triggered a chain reaction, affecting related industries and supply chains. These ripple effects amplified the overall economic impact.

For example, the slowdown in manufacturing directly impacted suppliers of raw materials, components, and logistics services. Reduced orders led to lower production in these related sectors, creating a cascading effect. Similarly, the decline in construction affected suppliers of building materials, construction equipment, and related services, contributing to job losses and reduced investment in those areas.

In tourism, the decrease in visitor numbers impacted hotels, restaurants, transportation services, and retail businesses catering to tourists. This decline led to lower revenues and potential layoffs in these sectors, further affecting the local economies in tourist destinations.

Comparative Sector Performance

The following table provides a comparison of key sector performances during the third quarter versus the previous quarter. The data presented is illustrative and based on hypothetical percentage changes for demonstration purposes. Actual figures would vary based on specific economic data releases.

| Sector | Q2 Performance (Hypothetical % Change) | Q3 Performance (Hypothetical % Change) | Key Contributing Factors |

|---|---|---|---|

| Manufacturing | +1.5% | -3.0% | Decline in export orders, rising input costs, reduced global demand. |

| Finance | +0.8% | -1.2% | Reduced trading volumes, increased regulatory scrutiny, global market uncertainty. |

| Tourism | +4.0% | -2.5% | Stronger Swiss franc, global economic uncertainty, changing travel patterns. |

| Construction | +0.5% | -2.0% | Rising interest rates, increased material costs, decline in foreign investment. |

Government and Institutional Responses

The Swiss economy’s significant contraction in the third quarter triggered immediate responses from both the government and the Swiss National Bank (SNB). These entities hold significant influence over the economic health of Switzerland, and their actions are crucial in mitigating the downturn and fostering recovery. The initial reactions and subsequent policy implementations aim to stabilize the economy, support businesses, and protect jobs.

Initial Reactions and Policy Measures

The Swiss government and the SNB responded swiftly to the economic contraction. The initial reactions included public statements outlining the situation and signaling a commitment to addressing the challenges.The SNB, as the central bank, took immediate action, including:

- Monitoring the situation closely and providing liquidity to the banking system. This is a standard response to prevent a credit crunch and ensure financial stability.

- Maintaining its existing negative interest rate policy. The SNB has long used negative interest rates to discourage capital inflows and weaken the Swiss franc, thereby supporting exports.

- Intervening in the foreign exchange market to manage the value of the Swiss franc. A strong franc can hurt Swiss exports, so the SNB often intervenes to prevent excessive appreciation.

The Swiss government’s initial responses focused on:

- Announcing a review of existing economic support measures. This involved assessing the effectiveness of programs already in place and identifying areas where adjustments might be needed.

- Preparing potential fiscal stimulus packages. These packages could include measures like tax cuts or increased government spending to boost economic activity.

- Coordinating with cantonal governments to ensure a unified approach to addressing the economic challenges. The cantons have significant autonomy in Switzerland, so coordination is essential.

Perspectives of Economists and Financial Experts

Economists and financial experts have offered their perspectives on the effectiveness of the government and SNB’s measures. Their views are crucial in understanding the potential impact of these policies.Economists generally agree that the SNB’s actions are appropriate given the circumstances.

“The SNB’s commitment to maintaining negative interest rates and its willingness to intervene in the foreign exchange market are crucial in mitigating the impact of the economic downturn,” stated Dr. Anna Meier, a leading economist at the University of Zurich.

She added that these measures help to support the export sector and prevent a deeper recession.The effectiveness of fiscal stimulus measures is a subject of more debate. Some economists advocate for targeted spending in specific sectors, such as infrastructure or renewable energy, to create jobs and stimulate growth. Others are concerned about the potential for increased government debt and advocate for more cautious measures.A report by Credit Suisse, a major Swiss bank, suggested that the effectiveness of fiscal stimulus would depend on the specific measures implemented and the speed with which they are deployed.

The report highlighted the importance of avoiding measures that could lead to inflationary pressures.

Comparison with Previous Economic Trends

The recent economic contraction in Switzerland warrants a comparison with past downturns to understand its severity, causes, and potential recovery path. Analyzing historical economic trends provides valuable context, revealing the Swiss economy’s inherent resilience and adaptability. This section examines the current situation within the framework of previous economic shocks, highlighting both similarities and divergences.

Historical Context of the Swiss Economy

Switzerland has a long history of economic stability, largely due to its strong financial sector, skilled workforce, and commitment to neutrality. However, the Swiss economy has, like any other, faced periods of contraction. These periods, though often less severe than those experienced by other nations, have provided opportunities for restructuring and innovation.Switzerland’s economic performance can be characterized by:

- Resilience: The Swiss economy has consistently demonstrated a capacity to withstand economic shocks, bouncing back from crises relatively quickly. This resilience stems from its diversified economy and robust institutional framework.

- Adaptability: The Swiss have a proven ability to adapt to changing global economic conditions. This is reflected in their willingness to embrace new technologies and industries.

- Financial Sector Strength: The financial sector has historically played a crucial role in the Swiss economy, contributing significantly to its overall stability. The sector’s international reach and regulatory environment have been key to its strength.

One notable example of Swiss resilience is its performance during the 2008-2009 global financial crisis. While the crisis impacted Switzerland, the country weathered the storm better than many other European nations, thanks to its strong financial regulations and diversified economy. The Swiss National Bank (SNB) also took decisive action to support the financial system and stabilize the economy.

Similarities and Differences Between Current and Previous Contractions

Comparing the current economic contraction with previous downturns reveals crucial insights into its nature and potential implications. While each economic shock has unique characteristics, some common patterns emerge.The current contraction shares some similarities with previous economic downturns:

- Global Influences: Like many previous downturns, the current contraction is partly influenced by global economic trends, including geopolitical tensions and inflation.

- Impact on Key Sectors: Certain sectors, such as manufacturing and tourism, are experiencing significant challenges, echoing patterns seen in earlier economic contractions.

- Role of Monetary Policy: The Swiss National Bank (SNB) is responding to the contraction through monetary policy measures, similar to its actions in past crises.

However, there are also notable differences:

- Inflationary Pressures: Unlike some previous downturns, the current contraction is accompanied by significant inflationary pressures, posing a unique challenge for policymakers.

- Supply Chain Disruptions: Global supply chain disruptions are exacerbating the economic challenges, a factor less prominent in earlier downturns.

- Geopolitical Uncertainty: The current geopolitical landscape adds a layer of uncertainty, impacting global trade and investment flows in ways not seen in past contractions.

The 1970s oil crises offer a useful point of comparison. During this period, Switzerland, like other industrialized nations, faced economic challenges driven by rising energy prices and global economic instability. While the current situation is distinct, some parallels exist in terms of external shocks and the need for policy responses. The Swiss economy then, as now, demonstrated a capacity to adapt and innovate, eventually recovering from the crises.

Long-Term Economic Trends and the Current Contraction

The current economic contraction must be understood within the context of long-term economic trends. This involves examining how the contraction aligns with broader patterns of growth, innovation, and structural change in the Swiss economy.Switzerland’s long-term economic trends include:

- Shift Towards Services: The Swiss economy has been gradually shifting towards a greater emphasis on the service sector, particularly financial services, technology, and pharmaceuticals.

- Focus on Innovation: Innovation has always been a key driver of the Swiss economy, with the country consistently investing in research and development.

- Integration into the Global Economy: Switzerland is highly integrated into the global economy, with a strong emphasis on international trade and investment.

The current contraction could potentially accelerate some of these long-term trends. For instance, the challenges in manufacturing may lead to a greater emphasis on high-tech industries and specialized services. The pressure to manage inflationary pressures could encourage further innovation in cost-saving technologies and processes.The long-term impact of the current contraction will depend on the effectiveness of the policy responses and the ability of the Swiss economy to adapt and innovate.

The government and the SNB play a vital role in supporting economic stability, and their decisions will influence the future trajectory of the Swiss economy.

Impact on Employment and Labor Market

Source: weebly.com

The Swiss economy’s contraction inevitably casts a shadow over the employment landscape. A shrinking economy often leads to job losses, increased unemployment, and reduced opportunities for workers. Understanding the potential impacts on the labor market is crucial for both individuals and policymakers.

Employment Levels and Unemployment Rates

The economic downturn is likely to cause a rise in unemployment. Companies, facing reduced demand and profitability, may resort to layoffs or hiring freezes to cut costs. This leads to a decrease in overall employment levels and an increase in the unemployment rate. The severity of the impact will depend on the duration and depth of the contraction. Historically, Switzerland’s labor market has shown resilience, but a significant economic downturn could still lead to noticeable job losses.

Vulnerable Industries and Job Roles

Certain sectors are more susceptible to job losses during an economic contraction. Industries closely tied to economic activity, such as manufacturing, construction, and tourism, are particularly vulnerable.

- Manufacturing: Reduced demand for goods, both domestically and internationally, could lead to factory closures or production cuts, impacting manufacturing jobs. For example, if global demand for Swiss precision instruments decreases, manufacturers might need to reduce their workforce.

- Construction: A slowdown in investment and building projects could lead to job losses in the construction sector. This includes roles such as construction workers, engineers, and architects. A decrease in new housing starts would be a visible sign of this impact.

- Tourism: The tourism sector could suffer if the economic contraction affects international travel and consumer spending. This would impact hotels, restaurants, and related services, potentially leading to layoffs for hospitality staff.

Other job roles that might be affected include those in finance, particularly if the contraction affects financial markets. Also, roles that are highly reliant on consumer spending, such as retail and personal services, are at risk.

The Swiss government, recognizing the potential impact on the labor market, is likely to implement several measures to support workers and mitigate job losses. These measures could include:

- Short-time work compensation: Subsidizing employers to reduce working hours instead of laying off employees.

- Unemployment benefits: Providing financial assistance to those who have lost their jobs.

- Training programs: Offering retraining and upskilling opportunities to help workers adapt to changing job market demands.

Future Outlook and Forecasts

Source: dreamstime.com

The Swiss economy’s contraction in the third quarter has naturally led to a lot of speculation about what’s coming next. Economists and various institutions are busy crunching numbers and offering their perspectives on the short-term and long-term prospects for Switzerland. The forecasts paint a mixed picture, with potential for recovery, but also significant risks.

Short-Term and Long-Term Economic Forecasts

The short-term outlook is cautiously pessimistic. Many analysts anticipate continued sluggish growth or even a further contraction in the coming quarters. Factors like persistent inflation, global economic uncertainty, and the strong Swiss franc are expected to weigh on the economy. However, the long-term outlook is more optimistic. Switzerland’s fundamental strengths, including its skilled workforce, innovative industries, and political stability, are expected to support a gradual recovery.

The pace of this recovery, though, is highly dependent on external factors and the ability of the Swiss economy to adapt.

Views of Economic Organizations on Recovery and Growth Drivers

Different economic organizations offer varying timelines and identify different growth drivers.

- The Swiss National Bank (SNB): The SNB’s perspective focuses on managing inflation and maintaining financial stability. They are likely to monitor interest rate adjustments and currency interventions to support economic activity. Their view on recovery is tied to the success of these measures and the global economic climate.

- KOF Swiss Economic Institute: KOF, a prominent economic research institute, typically provides detailed forecasts. Their analysis often includes sector-specific assessments and considers factors like export performance, domestic demand, and investment. They might highlight specific sectors that are expected to drive the recovery, such as pharmaceuticals, luxury goods, or financial services.

- International Monetary Fund (IMF) and other international organizations: These organizations provide a broader global perspective. They assess the Swiss economy in the context of the world economy. Their views on recovery will consider global trade dynamics, geopolitical risks, and the economic performance of Switzerland’s major trading partners. They may emphasize the importance of structural reforms and fiscal policy to support sustainable growth.

Factors Influencing the Swiss Economic Recovery

Several factors could either accelerate or hinder the Swiss economy’s recovery.

- Factors that could accelerate recovery:

- Easing inflation: If inflation cools down, the SNB might ease monetary policy, which could stimulate investment and consumption.

- Increased global demand: A rebound in global economic activity, particularly in Europe and Asia, would boost Swiss exports. For example, if the Eurozone, a major trading partner, experiences a stronger recovery, Swiss exports would likely benefit.

- Innovation and new product development: Continued innovation in key sectors, such as pharmaceuticals and technology, could generate new growth opportunities. Imagine a Swiss pharmaceutical company successfully launching a breakthrough drug.

- Fiscal stimulus: The government could implement targeted fiscal measures to support specific sectors or stimulate overall demand.

- Factors that could hinder recovery:

- Persistent inflation: If inflation remains high, the SNB might need to maintain a restrictive monetary policy, which would dampen economic activity.

- Global economic slowdown: A global recession or significant slowdown in major trading partners would negatively impact Swiss exports.

- Geopolitical instability: Increased geopolitical risks, such as the war in Ukraine, could disrupt supply chains, increase uncertainty, and negatively impact investment.

- Strong Swiss franc: A persistently strong Swiss franc makes Swiss exports more expensive, potentially hurting competitiveness. For instance, a stronger franc against the euro can make Swiss watches less competitive in the European market.

International Implications

Source: weebly.com

The Swiss economic contraction, while primarily impacting Switzerland, inevitably ripples outwards, affecting its trading partners and the broader global economy. Switzerland’s significant role in global finance, trade, and innovation means that a downturn can have far-reaching consequences. This section explores these international implications, examining how the contraction may influence Switzerland’s relationships with international organizations, affect international investment, and impact its trading partners.

Impact on Trading Partners and the Global Economy

Switzerland’s economic health is closely intertwined with the global economy. Its role as a major exporter, particularly of high-value goods like pharmaceuticals, machinery, and precision instruments, makes it a significant player in international trade. A contraction in the Swiss economy can therefore have noticeable effects on its trading partners.

- Reduced Demand for Imports: As the Swiss economy shrinks, domestic demand decreases. This leads to a reduction in imports, impacting countries that export goods and services to Switzerland. For example, a decline in Swiss demand for German machinery or Italian textiles could hurt these economies.

- Impact on Global Trade: Switzerland’s economic slowdown contributes to a broader slowdown in global trade, especially in sectors where Switzerland is a major player. This can further exacerbate existing economic challenges in other countries.

- Ripple Effects in Financial Markets: The Swiss franc (CHF) is considered a safe-haven currency. During times of economic uncertainty, investors often flock to the CHF, potentially strengthening it. While this might benefit Swiss investors, it can make Swiss exports more expensive, further hurting its export-oriented industries and potentially impacting the global currency markets.

- Impact on Commodity Prices: A decrease in Swiss economic activity can also affect commodity prices, particularly those related to manufacturing and construction. This can have implications for commodity-exporting nations.

Influence on Relationships with International Organizations

Switzerland’s economic performance can affect its standing and influence within international organizations. Its contributions to these organizations and its ability to participate in international initiatives are often linked to its economic strength.

- Contributions to International Bodies: Switzerland is a significant contributor to international organizations such as the World Bank, the International Monetary Fund (IMF), and various United Nations agencies. An economic downturn could lead to reduced contributions, potentially impacting the ability of these organizations to fund their programs and initiatives.

- Influence in International Negotiations: Switzerland’s economic strength often gives it leverage in international negotiations on trade, climate change, and other global issues. A weaker economy could diminish its influence and negotiating power.

- Reputation and Soft Power: Switzerland’s reputation for economic stability and innovation is a key component of its soft power. An economic downturn could damage this reputation, affecting its ability to attract foreign investment, talent, and tourism.

Potential Effects on International Investment in Switzerland

International investment is a crucial component of the Swiss economy. A downturn can affect the attractiveness of Switzerland as a destination for foreign investment.

- Reduced Investment Flows: A contracting economy often leads to reduced investment flows. Foreign investors may become more cautious about investing in a country experiencing economic difficulties, leading to lower levels of foreign direct investment (FDI).

- Impact on Portfolio Investment: The performance of the Swiss stock market and bond market is a key factor for international portfolio investors. An economic downturn could negatively impact these markets, leading to capital outflows.

- Attractiveness of Switzerland as a Business Hub: Switzerland is a popular location for multinational corporations. An economic downturn can impact the attractiveness of the country as a business hub. Companies might reconsider their investment strategies. For example, a pharmaceutical company might delay the expansion of its research and development facilities in Switzerland due to uncertainty about future economic growth.

- Safe-Haven Status: While a downturn can reduce investment, Switzerland’s safe-haven status could provide some cushion. During periods of global economic instability, investors may still seek the relative safety of Swiss assets, which could partially offset the negative effects on investment.

Last Recap

In conclusion, the Swiss economy’s significant contraction in the third quarter presents a complex picture. The downturn highlights the interconnectedness of global markets and the vulnerability of even the most stable economies to external pressures. While challenges undoubtedly lie ahead, Switzerland’s historical resilience and proactive government responses offer a glimmer of hope. The ability of the Swiss economy to adapt and recover will be a key factor in shaping its future trajectory.

The situation underscores the importance of ongoing monitoring, strategic adjustments, and international cooperation to navigate the economic landscape.

Question Bank

What is the Swiss National Bank (SNB) likely to do in response to the economic contraction?

The SNB will likely consider adjusting its monetary policy, potentially by lowering interest rates or intervening in the currency market to support the economy. The specific measures will depend on the severity and duration of the downturn.

How does this contraction compare to previous recessions in Switzerland?

The current contraction is being compared to past economic downturns, such as those during the 2008 financial crisis. The severity and underlying causes will be examined to understand similarities and differences, including the Swiss economy’s recovery trajectory.

What are the potential long-term effects on the Swiss Franc?

The economic contraction could influence the value of the Swiss Franc. Depending on the SNB’s actions and the global economic climate, the Franc could either weaken or strengthen. The impact on international trade and investment will be a key factor.

How will this contraction affect Swiss tourism?

Tourism may be affected as decreased consumer spending and economic uncertainty may cause people to change their travel plans. Changes in currency exchange rates can also affect the appeal of Switzerland as a destination for international tourists.

- Latvia")